DO RETAILERS NEED TO WORRY ABOUT AIM ACT COMPLIANCE UNDER TRUMP?

- Amrit Robbins

- Jan 20, 2025

- 4 min read

Updated: May 28

Key Takeaways

Project 2025 proposed repealing unnecessarily stringent HFC regulations, raising questions about AIM Act enforcement under a Trump administration.

Despite deregulatory signals, the AIM Act has bipartisan support and its final rules are embedded in federal law — repeal is extremely unlikely.

Retailers who pause compliance planning due to political uncertainty are taking a high-risk bet with significant financial downside.

The safer strategic posture is to proceed with compliance regardless of political environment — the ROI on leak detection stands on its own.

California CARB refrigerant rules operate independently of the AIM Act — state enforcement continues regardless of federal deregulatory moves, and the CARB RMP is stricter on almost every dimension.

Project 2025, a conservative policy blueprint for a potential Republican administration, has raised questions about the future of HFC regulations under the American Innovation and Manufacturing (AIM) Act. While the document calls for repealing "unnecessarily stringent and costly" HFC regulations, grocery retailers should think carefully before delaying their compliance preparations. The business case for improved refrigerant management extends far beyond regulatory requirements, and the AIM Act itself rests on remarkably stable ground.

Does the Trump administration’s deregulatory agenda apply to the AIM Act’s refrigerant leak detection requirements?

Let's first consider the political reality. The AIM Act passed with strong bipartisan support in 2020, co-sponsored by 17 Republican senators and signed into law by President Trump himself. The law garnered broad industry backing, with support from major trade organizations including the American Chamber of Commerce, ASHRAE, and AHRI, along with leading refrigerant suppliers like Honeywell and Chemours, and equipment manufacturers such as Danfoss, Daikin, and Carrier. This widespread support reflects a crucial reality: coordinated federal regulation is far preferable to a patchwork of state requirements.

📊 Stat: The AIM Act was codified by Congress and cannot be reversed by executive order alone. The EPA finalized Subpart C in October 2024. The 60-day Congressional Review Act window expired before any rollback effort could succeed. Compliance remains legally required regardless of administration. (Source: Congress.gov / EPA)

What is the legal risk to grocery retailers who delay AIM Act compliance waiting for a potential rollback?

Prior to the AIM Act's passage, approximately 20 U.S. states had advanced their own measures to regulate HFC refrigerants. Many suspended these initiatives when federal regulation took effect. If federal enforcement were to weaken, these state-level regulations would likely resurface quickly. For multi-state operators, navigating this complex web of varying requirements could prove far more costly than meeting a single federal standard.

How has Congress protected AIM Act Subpart C from executive reversal?

Even if Project 2025's recommendations were fully implemented, several factors would protect the AIM Act's core provisions. The law's phasedown schedule mirrors international commitments under the Kigali Amendment, which the Senate ratified with bipartisan support. Major chemical companies have already invested heavily in next-generation refrigerants, creating a powerful industry constituency for maintaining the transition. Additionally, the EPA can investigate violations retrospectively for three or more years, meaning non-compliance during any period creates significant potential liability - including fines of in the tens of thousands of dollars per day and possible jail time - that could be enforced by future administrations. Taking such a massive financial and legal risk based on speculation about future enforcement would be difficult to justify to shareholders, board members, and other stakeholders.

But perhaps most importantly, focusing solely on potential regulatory changes misses the compelling business case for improved refrigerant management. The average grocery store loses about 25% of its refrigerant annually, with each leak driving up costs through emergency repairs, increased energy consumption, and potential product loss. With grocery stores operating on razor-thin margins of 1-2%, these losses represent a significant drain on profitability that exists regardless of regulatory requirements.

Consider the financial implications of refrigeration failures. When systems fail, the biggest impact is often lost sales and customer loyalty. According to an Ipsos survey, nearly one in four shoppers (23%) will shop at a different store next time if just 1-3 items from their list are unavailable. With perishable goods accounting for 51% of all grocery sales, a refrigeration outage can drive away customers permanently. Beyond these critical lost sales, stores face direct repair expenses, disrupted operations, diverted staff time, and inventory losses. Every hour employees spend dealing with refrigeration issues instead of serving customers represents lost productivity and revenue. In an industry with razor-thin margins, losing even a small percentage of repeat customers due to refrigeration failures can have devastating long-term financial consequences.

Energy costs present another compelling reason for proactive refrigerant management. Energy is typically the second-highest operating expense for supermarkets, with refrigeration accounting for a substantial portion. Systems operating with undetected leaks consume more energy, driving up utility bills month after month. The National Renewable Energy Laboratory has identified refrigeration efficiency as a key opportunity for reducing national energy consumption.

Looking ahead, market forces will continue driving changes in refrigerant management regardless of regulatory enforcement. The global phasedown of HFC production and imports means refrigerant costs will likely continue rising. Supply chain dynamics and growing investor focus on environmental performance will further incentivize better refrigerant management practices. Early adopters of comprehensive leak detection systems will be better positioned to manage these increasing costs while maintaining operational efficiency.

For grocery retailers weighing their options, the timing of implementation matters. As the January 2026 enforcement deadline approaches, demand for automatic leak detection systems will likely surge, potentially driving up costs and extending installation timelines. Early adopters can avoid this rush, securing better pricing and preferred installation schedules that align with their operational needs.

The most successful retailers will recognize that this isn't about politics or even compliance – it's about embracing best practices that protect profitability, minimize risk, and position their businesses for long-term success. Whether motivated by operational efficiency, cost reduction, environmental responsibility, or risk management, the business case for improved refrigerant management remains strong regardless of the political landscape.

In an industry where margins are thin and competition is fierce, waiting to implement these systems means leaving money on the table. The question isn't whether to implement these systems, but rather how quickly retailers can begin realizing the benefits of improved refrigerant management. Those who act early will gain a competitive advantage, while those who wait risk falling behind – both operationally and financially.

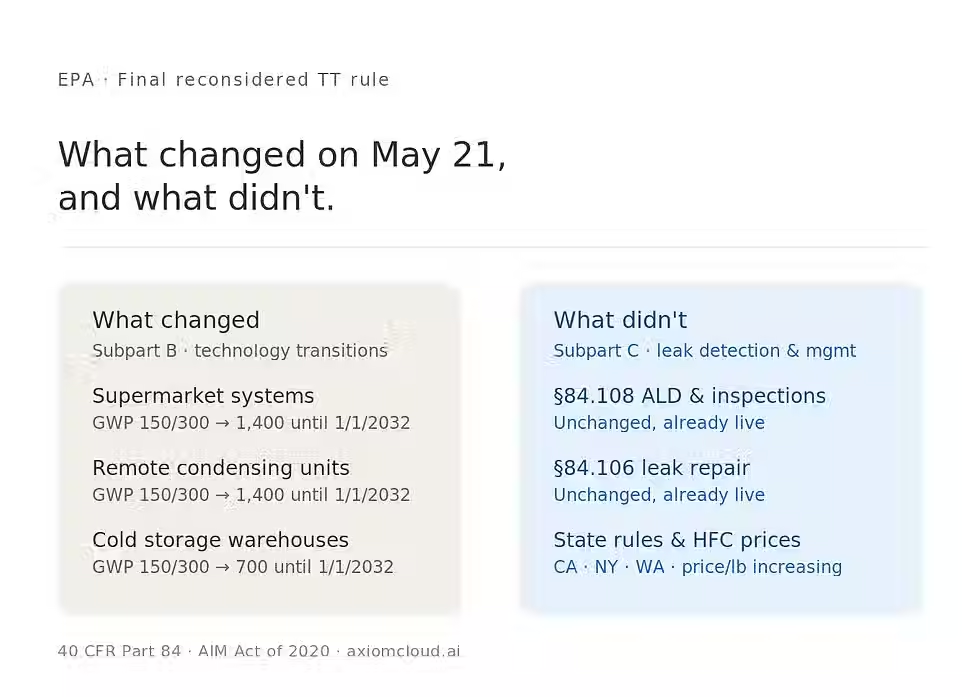

The May 2026 TT Reconsidered Rule confirmed it: ALD requirements under §84.108 are unchanged. Our pillar guide on refrigerant leak detection covers what the post-reconsideration landscape actually looks like for retailers.

Comments